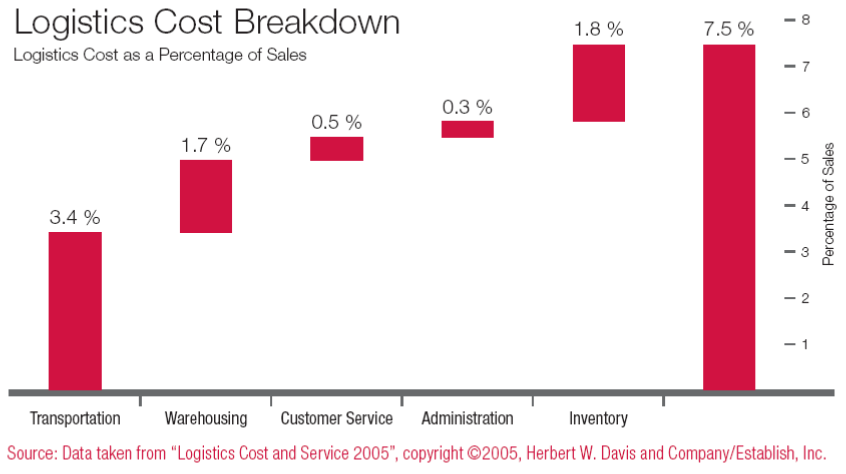

Inventory value

4

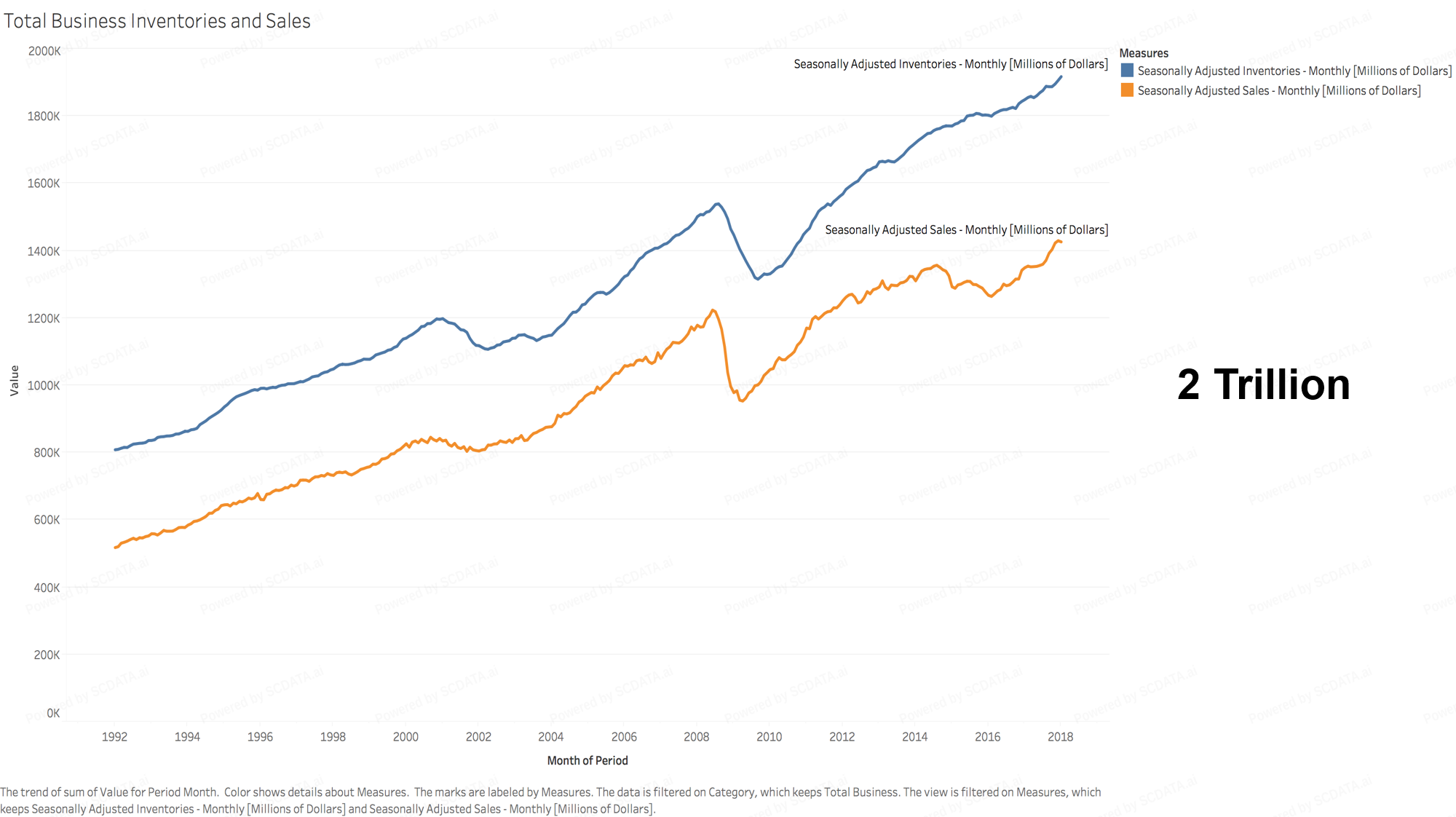

US census data. We plot monthly sales (orange line) and inventory (blue line) from 1992 to 2018 for the US. As we can see, except for the drop around year 2009 due to the financial crisis, both sales and inventory are growing. Up to 2018, we carry about 2 Trillion dollars of inventory.

4/37

Inventory trend

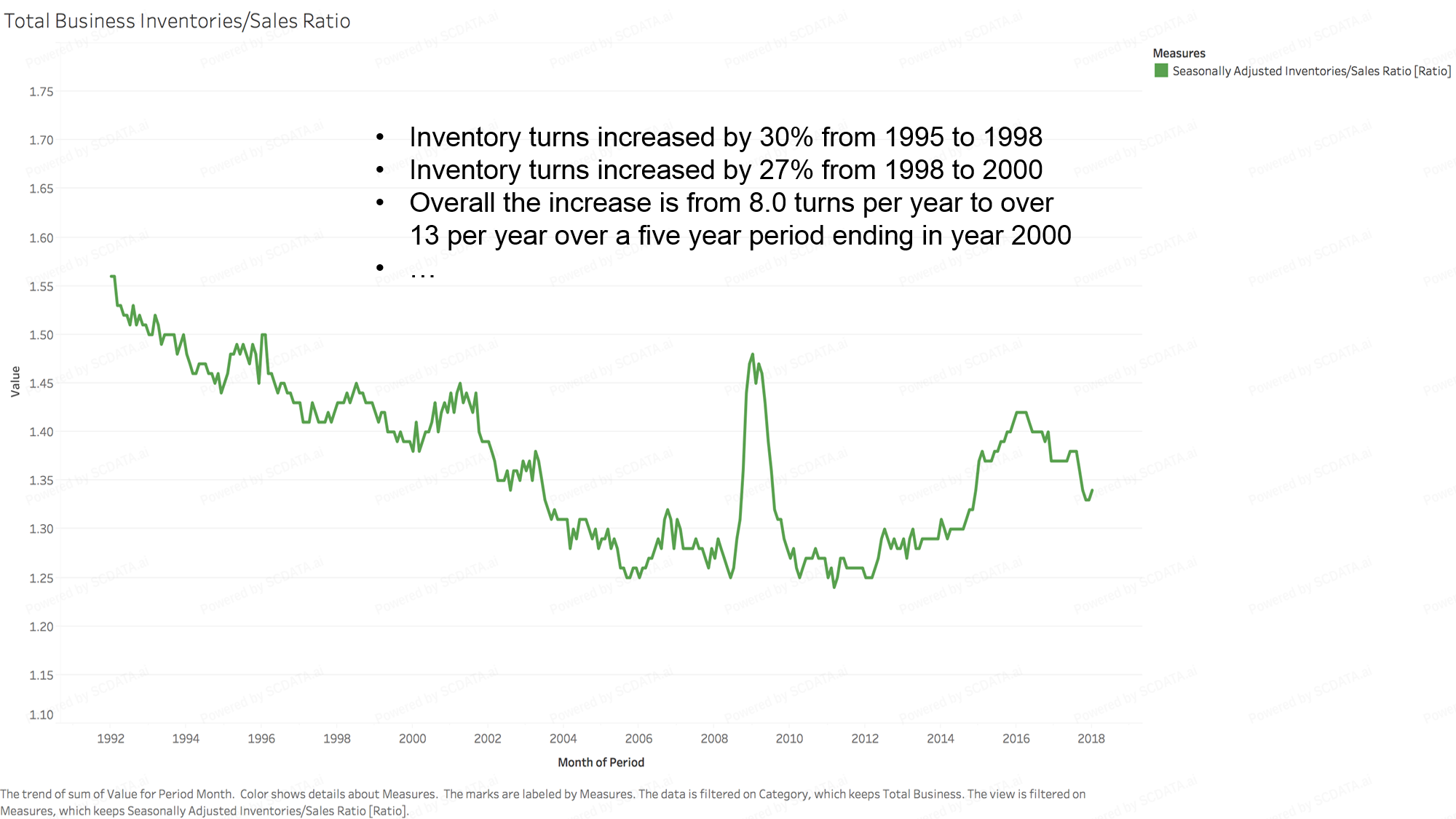

5

We plot the inventory over sales ratio, which is an indicator of inventory efficiency. The lower the ratio, we need less inventory to meet the same demand, which means a higher inventory efficiency. For the same time period, we found that the inventory efficiency was improving constantly up to 2008, but was disrupted by the financial crisis. Afterwards, inventory efficiency was dropping.

5/37

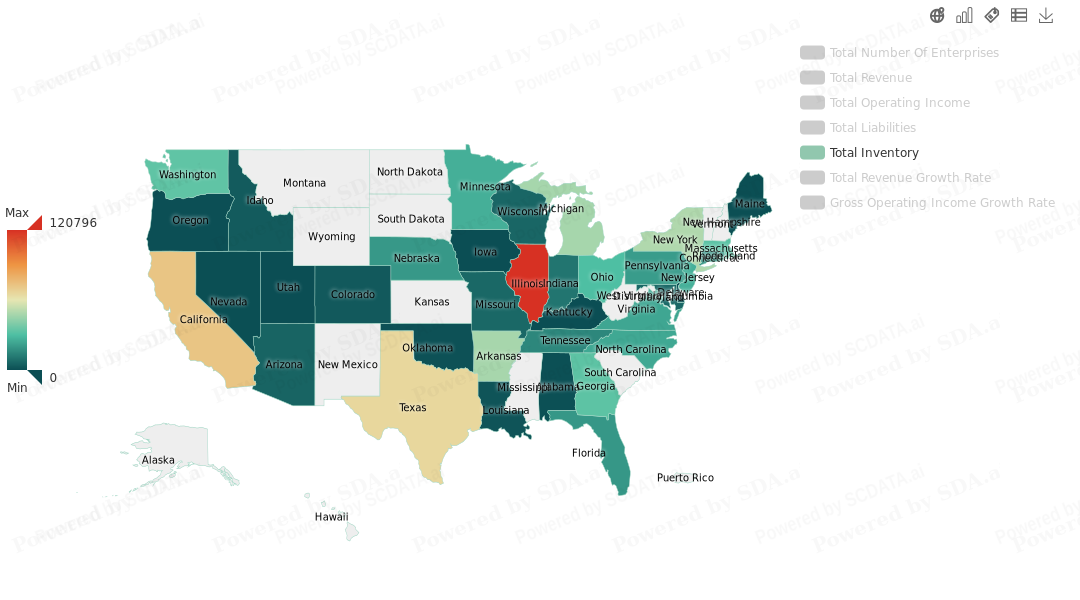

Where is inventory in the US?

7

In the US, firms headquartered in IL carry the most inventory

7/37

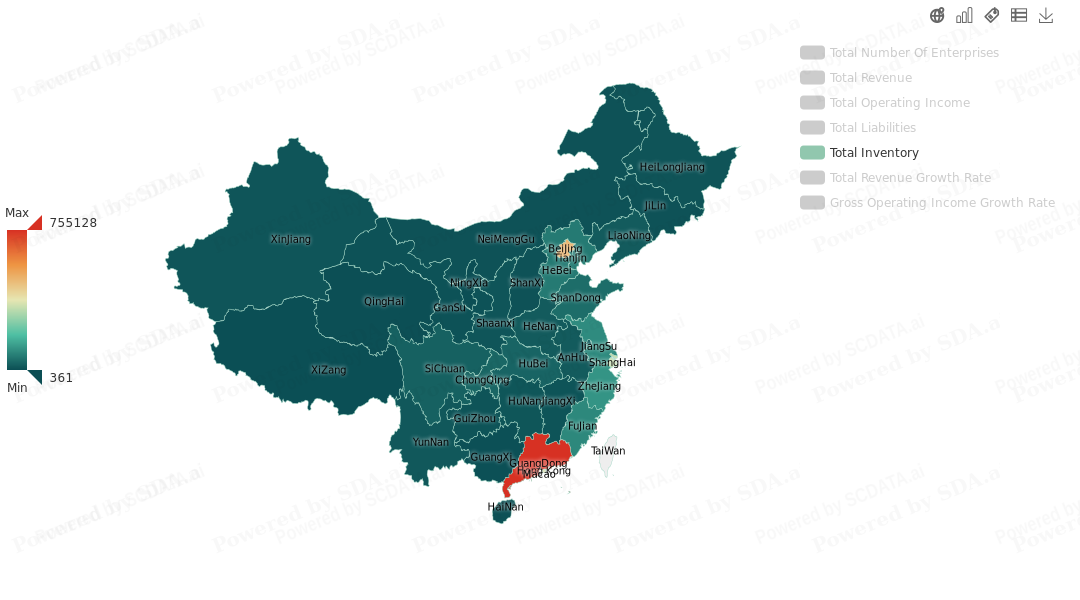

Where is inventory in China?

8

In China, firms headquartered in Guangdong carry the most inventory.

8/37

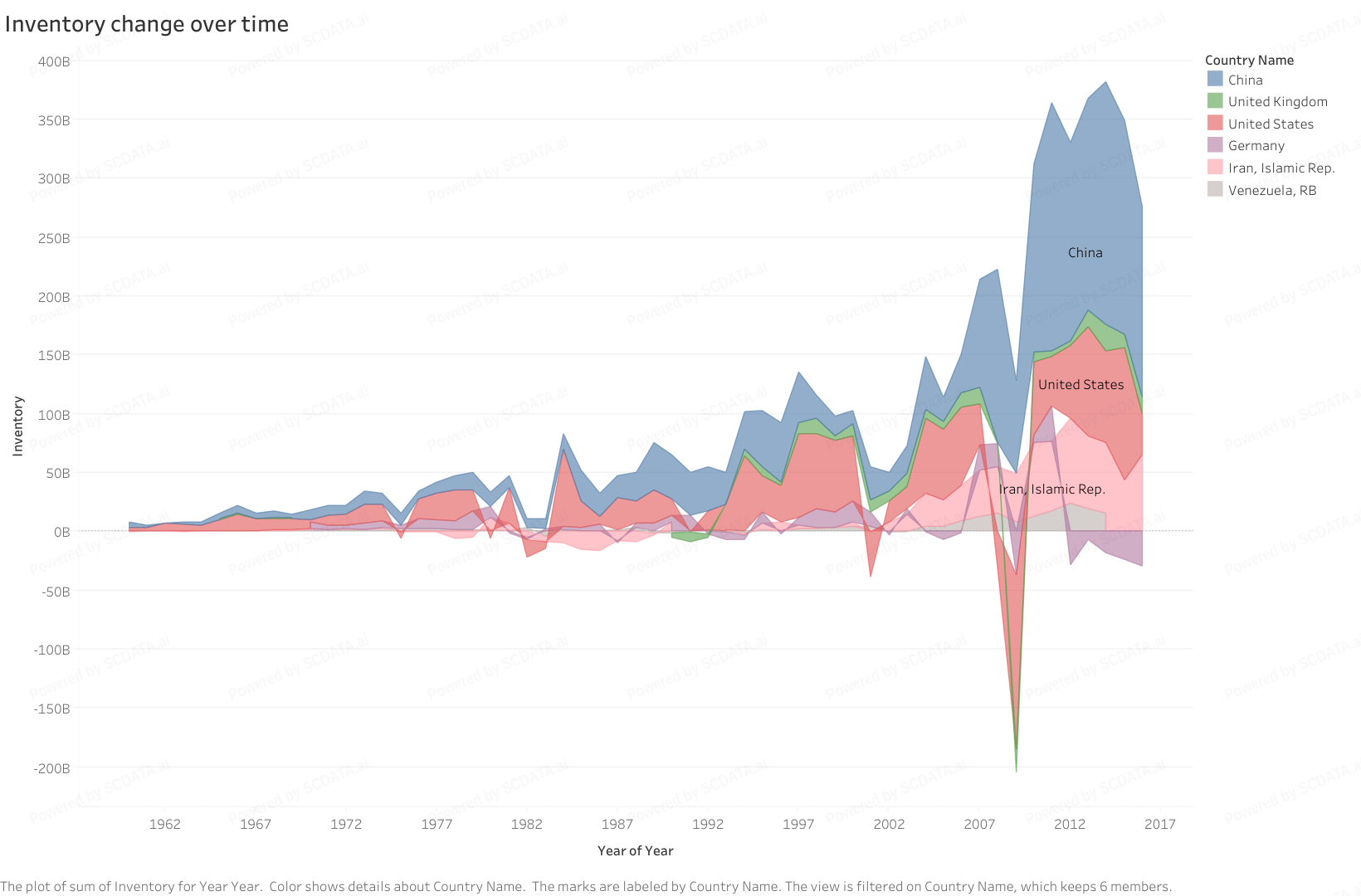

Inventory economic indications

9

The World Bank data on inventory changes provides many interesting indications on the world’s major economies.

1. China’s inventory changes follow the pattern of the US but are slightly lagged behind and much more dramatic than the US in recent years, part of the reason is that China was supplying US.

2.The times of major economic recessions coincide well with the negative changes of inventory. In fact, a significant and negative change of inventory is a strong indicator of economic recession.

3.The changes are swinging bigger and bigger as time goes by, with an almost exponential growth.

4.Germany has a different pattern from the US – a significant and consistent reduction of inventory in recent years, indicating a very different industrial practice on inventory management.

9/37

Benchmark by KPI - US, 2018

11

Let’s first look at the US. The table shows inventory over total asset for different level 1 industry sectors in year 2018. We can see that companies in the industry sectors of materials, industrials, consumer discretionary, consumer staples, healthcare and IT have a sizable asset in inventory. In particular, the median firm in consumer discretionary (such as autos, apparel, home appliances, and retail) has 17% of asset in inventory, and the 90th percentile has 47% of its asset in inventory. Although the median of IT firms is only 4%, the 90th percentile can go up to 16%. So for these industries, inventory simply cannot be ignored!

11/37

Benchmark by KPI - China, 2018

12

For China, the table looks a bit different: In addition to the industry sectors of materials, industrials and so on, it looks like real estate in China has the highest percentage of asset in inventory with a median of 41%!

12/37

Benchmark by KPI - Inventory / Total Asset, level 2

13

In order to take a closer look at the industries with a high % of asset in inventory, we drill deeper into a finer classification of industries for the US, that is, the level 2 industry groups, where we pick capital good, food staples retailing, retailing and food beverage Tobacco and so on. As we can see, retailing (such as department stores) has the highest percentage of asset in inventory with a median of 30%. Food & Staples retailing (such as discounted stores like WMT, COSTCO, etc.) is the second highest with a median of 18%, this is followed by consumer durables and apparel (the median is 17%), household and personal products (10%) and so on.

13/37

Benchmark by KPI - China, level 2

14

Let’s do the same analysis for China, and we found that the number one industry in inventory over total asset ratio is real estate (the median 41%), and it is followed by consumer durables and apparels (the median is 15%), and capital goods (such as airplanes, heavy machinery), food staples retailing, retailing, and so on.

14/37

Industrial Comparison (excluding financials) for US

17

We selected all level 1 industries and year 2018. The analysis compares these industries on cost efficiency, labor productivity, inventory turns and market power. The bottom left graph shows that healthcare has the lowest inventory turns, which is followed by consumer discretionary, materials, IT, consumer staples and so on. It is interesting to note that real estate in the US has an inventory turns of 17 a year for the median.

17/37

Industrial Comparison (excluding financials) for China

18

The pictures in China look completely different. In 2018, real estate in China has a median inventory turn of about 0.27, which is equivalent to about 1300 days of inventory! You can observe other interesting things such as labor productivity defined to be revenue over # of employees, china is much lower on labor productivity than the US in all industry sectors.

18/37

Industrial Trend: China vs US on real estate efficiency

19

Now let’s take a closer look at the inventory days for real estate in China. The graph on the top left corner shows that China’s real estate industry carries way too much inventory with a median inventory days to be more than 1200 days. Consequently, the median cash conversion cycle is in the range of 600 to 800 days, as shown by the top right graph. The graphs on the bottom show that the asset turnover and return on asset are comparable for real estate industries between US and China.

19/37

Industrial Trend: China vs US on retailing efficiency

20

US retailing carries more inventory than China but has a higher asset turnover and ROA due to a higher margin.

20/37

Industrial Trend: China vs US for retailing profitability

21

US retailing is much more profitable than China on all profit margins, such as gross margin, operating margin and net margin.

21/37

Value Driver Analysis: inventory turnover vs operating cost / revenue, retail, USA

23

We select the retailing industry, for example, and years from 2016 to 2018. We observe that as inventory turnover increases, the operating cost over revenue ratio decreases for this industry, which implies that a higher inventory turnover may lead to a lower operating cost for retailing.

23/37

Value driver analysis: inventory turnover vs gross margin for retail, US

24

For the same analysis, we chose the y variable to be gross margin, and we found that, interestingly, as inventory turnover increases, the gross margin may decrease, which may come from a higher COGS for the products due to perhaps the loss of scale economies in buying less bulk.

24/37

Value Driver Analysis: inventory turnover vs asset turnover

25

As inventory turnover increases, the asset turnover increases for US retailing

25/37

Benchmark by KPI: inventory days, US selected industries

27

The analysis shows that the difference on inventory days can be huge for companies in the same industry. For US retailing, the median inventory days is around 90 days. The 90th percentile (the worst performing companies) is about 285 days and 5 times the 10th percentile (the best performing companies). The 90th percentile of consumer durables and apparel is even more dramatic with 372 days (more than one year of inventory) and the 10th percentile is only 59 days. Finally, the 90th percentile of food beverage tobacco is 235 days, so the products have sit in their warehouse for more than 200 days before reaching retailing firms, while the best performing companies (the 10th percentile) have only 38 days.

27/37

Enterprise Ranking by inventory days for US retailing

29

Amazon is the best with the smallest inventory days of 45 days. While Macy’s ranks 19th with an inventory days of more than 120 days.

29/37

Enterprise Comparison: Amazon vs Macy's on efficiency

30

Amazon outperforms Macy's in every dimension such as operating cost over total revenue ratio, cash conversion cycle, inventory days and asset turnover, except the receivable days / payable days ratio. Specifically, Macy's payable days is 10x its receivable days, and Amazon’s payable days is 4x its receivable days. This means Macy’s suppliers may have to wait a much longer time to get paid than Amazon’s suppliers.

30/37

Enterprise Comparison - Profitability

31

Amazon and Macy's gross margins are about the same.

31/37

Enterprise Comparison: Amazon vs Macy's on size

32

Amazon is much bigger than Macy's in every dimension

32/37

Enterprise Trend - Market Share

33

Amazon's revenue and operating income are growing rapidly while Macy's stays stagnant or is slowly decreasing.

33/37

Enterprise Trend on efficiency: Amazon vs Macy's

34

Amazon is more efficient and productive than Macy’s and treats suppliers better

34/37

KPI Examination for Amazon within retailing

35

Amazon: quite profitable, fine health, highest growth, very efficient

35/37

KPI Examination for Macy's within retailing

36

Macy's: less profitable, fine health, little growth, very inefficient.

36/37

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}